Celebrate the Facts!

|

|

|

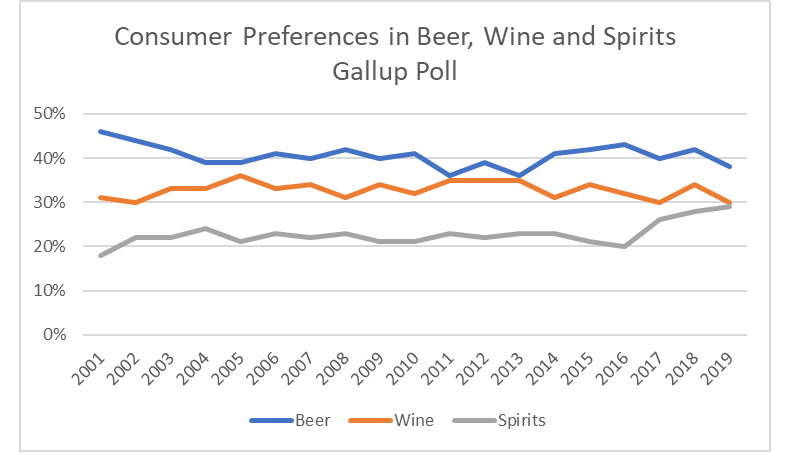

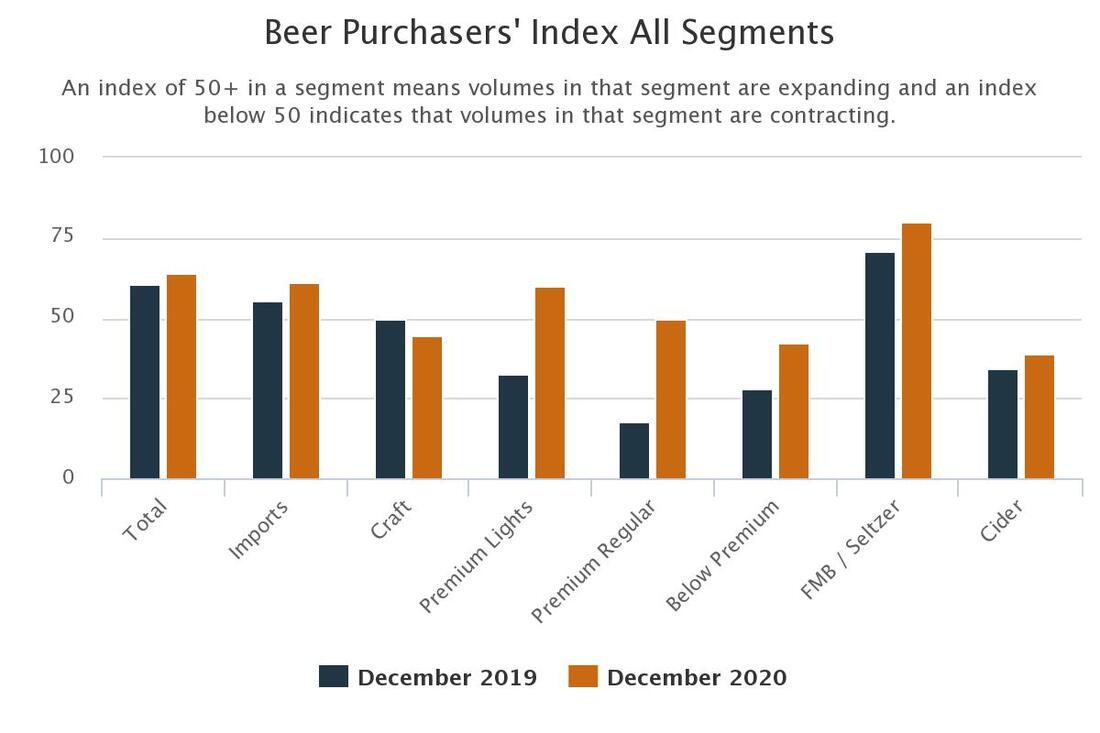

1/17/2021 2 Comments Big Beer is Back AgainBeer, the perennial alcohol favorite choice of Americans, has been changing as overseas firms have taken over American-born brews such as Coors, Miller, and Budweiser. The erosion of the market share of these behemoths by craft beers has been heartening but is threatened by COVID. The pandemic’s societal tsunami will alter the beer business by strengthening iconic brands as at-home consumers are tending to experiment less and economize more.  Despite sentiments to the contrary beer is and has been the alcohol of choice by American consumers. United States citizens 21 years and older consumed about 26 gallons of beer per person in 2019. Beer sold in cans accounted for 60% of all beer sold, glass bottles 30%, and draft beer 10%. There were about 6,400 breweries in the United States in 2019, an increase of about 436 from 2018, and about 25% of these breweries were classified as brewpubs that only brew beer for direct-to-consumer sale on brewery premises. More than 95 percent of all breweries made fewer than 15,000 barrels (465,000 gallons) per year and only about 3 percent of the total volume of craft beer sold. United States beer volume sales were down 2% in 2019, whereas craft brewer sales continued to grow at a rate of 4% by volume, reaching about 14% of the U.S. beer market by volume. Retail dollar sales of craft beers increased 6%, up to about $29 billion, and were more than 25% of the $116 billion United States beer market, meaning the craft beers are more expensive per unit. The craft beer business has bloomed and provided a great deal of variety and uniqueness in a product selection formerly dominated by bland industrial lagers made from adjuncts. Classic beer was brewed by German national covenant with barley, hops, and water only but American mega-brewers used adjuncts -cheaper corn or other grains – much to the detriment of flavor. The rise of craft brewing provided American consumers with incredible variety and often superior quality, albeit at higher costs.  The effects of COVID on beer consumption have been substantial. The National Beer Wholesalers Association (NBWA) Beer Purchasers’ Index (BPI) is an informal monthly statistical release giving distributors an indicator of industry beer purchasing activity. The BPI is the primary forward-looking indicator for beer distributors to anticipate demand. Interesting conclusions can be drawn from this information:

The impact of COVID on the beer industry has been marked with on-premises sales diving due to closedowns. Aside from traditional bars, this has affected brewpubs to the extreme and will put the survival of many of these in jeopardy. Other changes include:

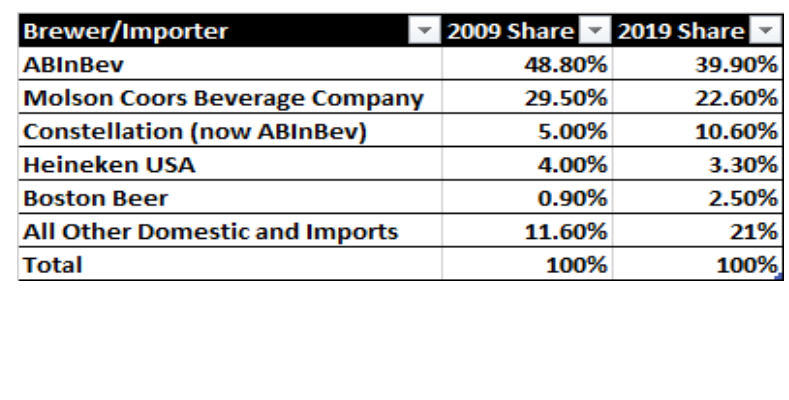

Market Share by Brewer 2009 and 2019 The classic definition of a brand is a person’s perception of a product, service, experience, or organization. The industrial brewers spend over $1 billion each year in the United States to protect and extend market share. The 10 most popular beer brands in the United States in 2019 were manufactured by two industrial brewers:

Regardless of the fragmented nature of the market, it is dominated by these two international brewing organizations. They can flex their muscles through traditional monopolistic practices including predatory pricing and distribution. Whether such dominance is a good or bad thing it seems depends on one’s tastes for beer.  The story of Pabst Blue Ribbon and other blue-collar brands such as Schlitz, Old Milwaukee, and Colt 45 followed a dissimilar amalgamation to foreign entities. These brewers, along with other iconic brews such as Old Style, were crushed by better capitalized mega-brewers Anheuser Busch and Miller. Pabst closed its Milwaukee brewery in 1996 after 152 years. Pabst is now owned by a holding company comprised of a Russian brewer in conjunction with a venture capital fund. Pabst Blue Ribbon is now available in Australia, Canada, Ukraine, Russia, and China. This organization creates zombie brands through buying the brand and logo, then by contracting the brewing to Molson Coors Beverage Company. The Pabst umbrella now owns brands formerly brewed by these entities:

About half of the beer produced under Pabst's ownership is the Pabst Blue Ribbon brand, with the other half divided among the other owned brands, occupying a niche market that might be defined as urban grunge chic. Pabst Blue Ribbon’s resurgence was due to its popularity with urban hipsters who appreciated the dollar-a-can promotion in certain bars and liked the beer's dissident understated image making it essentially a social protest brand. These were about freedom and rejecting middle-class mores, and Pabst Blue Ribbon was a symbol of this protest. Pabst Blue Ribbon is not a product that relies on its merits as a beer. The authoritative beer rating resource is ratebeer.com which is a crowd-rating site for beers. Pabst Blue Ribbon has a cumulative rating of 2.06 out of five with 3,391 ratings at the time of this investigation. By 2017 Pabst Blue Ribbon had become the 16th most popular beer, albeit in a fragmented market, as it had 2.5 million barrels sold, but only a 1.2% market share. Pabst Blue Ribbon and its sister brands are brewed under contract by the Molson Coors Beverage Company, a relationship that has become litigious as the Pabst brand family sales have grown, resulting in a recent court case intended by Molson Coors to end the relationship, settled at the 11th hour by an ‘amicable’ agreement. The Pabst organization agreed to purchase Molson Coors Beverage Company’s Irwindale, California brewery and so will be back in the own-and-operate business model. Owning and not contracting offers some disadvantages including tying up capital, extended distribution requirements, and the inability to ramp up or down easily to adjust to demand. Inevitably this will lead to higher prices. Statistical information on beer consumption can be found at https://www.brewersassociation.org/statistics-and-data/national-beer-stats/. The information about anticipated beer demand was obtained at https://www.nbwa.org/resources/beer-purchasers-index. The ABInBev brand line was provided by https://www.ab-inbev.com/. Information on the Pabst marketing strategy was obtained at https://archive.is/20130118070908/http://www.bloomberg.com/apps/news?pid=20601094&refer=book&sid=a6ZkYz6vWDD0. Documentation on the end of Pabst in Milwaukee was provided by https://www.nytimes.com/1996/11/06/us/brewery-s-exit-leaves-a-bitter-taste.html. More marketing of Pabst information was obtained at https://www.nytimes.com/2003/06/22/magazine/the-marketing-of-no-marketing.html?pagewanted=all.

2 Comments

Jeff Woynich

1/17/2021 08:10:49 pm

Holy Research Batman ! 2/2/2021 03:45:02 am

The Grainfather has a smooth appearance consisting of an excellent feature set. It will enable you to get an entirely new level of enjoyment with a basic and easy beer making maker in your home Leave a Reply. |

InvestigatorMichael Donnelly investigates societal concerns with an untribal approach - to limit the discussion to the facts derived from primary sources so the reader can make more informed decisions. Archives

July 2023

Categories |

RSS Feed

RSS Feed